According to TrendForce’s latest memory spot price trend report, the DRAM market is currently characterized by spot prices remaining above contract levels, while Q2 2026 pricing negotiations have yet to begin. As a result, a broad wait and see sentiment is prevailing across the market. At the same time, NAND Flash spot prices continue to trend upward, with 512Gb TLC wafers rising 14.7% this week, although buyers remain cautious.

Following the Lunar New Year holiday, the global memory market has entered a watchful phase. DRAM spot prices remain higher than contract prices, while pricing talks for Q2 2026 have not officially kicked off. Meanwhile, NAND Flash continues its upward trajectory, though real buying momentum has not fully accelerated.

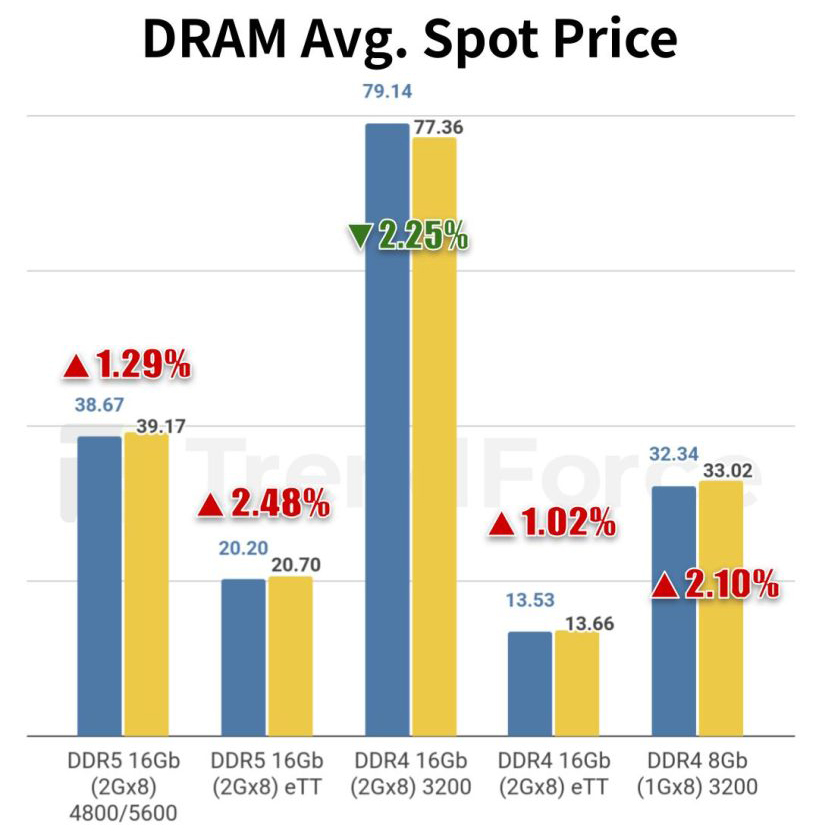

DRAM: Spot prices stay above contracts as wait and see sentiment dominates

The DRAM spot market has remained relatively subdued. Post holiday inquiry activity and quotations have been limited, reflecting cautious sentiment on both the buy and sell sides.

With current spot prices higher than contract prices and Q2 2026 negotiations not yet underway, the market is holding back to assess the next pricing benchmark. Trading activity remains defensive, with no strong signs of aggressive procurement.

TrendForce maintains its previous outlook that near term spot price increases will be relatively moderate, and the gap between spot and contract prices is expected to narrow gradually.

This week, the average spot price of mainstream DDR4 1Gx8 3200MT/s chips rose 2.10%, from US$32.34 to US$33.02, indicating a continued upward trend, though not a breakout surge.

NAND Flash: Up 14.7% but buying momentum still restrained

In the NAND Flash segment, price gains have been more pronounced. Ahead of the Lunar New Year, some traders liquidated inventory for cash flow purposes, leading to a brief dip in spot prices. However, the broader trend remains upward.

This week, spot prices for 512Gb TLC wafers increased by 14.70%, with average quotations surpassing US$20.586. The magnitude of this rise is notable given the market’s current cautious tone.

Despite the price rally, buyers continue to adopt a wait and see stance rather than engaging in aggressive purchasing. As a result, actual transaction momentum has weakened, raising questions about the sustainability of the recent price surge without large scale orders.

Outlook: Market awaits signals from Q2 negotiations

Overall, both DRAM and NAND markets are in a sensitive transition period ahead of Q2 2026 contract negotiations. Rising spot prices suggest improving supply demand dynamics, but market sentiment remains more observational than decisive.

The coming weeks, particularly the formal start of Q2 pricing negotiations, will be critical in determining the next benchmark for memory pricing in the first half of 2026.